In this article, I will address the Best Stocks or Sectors to Watch in European Banking and Finance. Europe has the ever-changing landscape of the world’s finance and offers the ability to invest in major world banks, firms in diversified finance, and Fintech.

- Key Points & Best Stocks or Sectors to Watch in European Banking & Finance

- 10 Best Stocks or Sectors to Watch in European Banking & Finance

- 1. Barclays (BARC.L)

- 2. UBS Group (UBSG.SW)

- 3. UniCredit (UCG.MI)

- 4. BNP Paribas (BNP.PA)

- 5. Commerzbank (CBKG)

- 6. Nordea Bank (Nordic Region)

- 7. Lloyds Banking Group (UK)

- 8. Crédit Agricole (France)

- 9. Société Générale (France)

- 10. ING Groep (Netherlands)

- How To Choose The Best Stocks or Sectors To Watch In European Banking & Finance

- Conclsuion

- FAQ

Europe’s Banking and Finance has top-performing banks, and we will explain the main components of the market along with the important aspects to look at in order to achieve the most shareholder value in the European Banking and Finance.

Key Points & Best Stocks or Sectors to Watch in European Banking & Finance

| Stock/Sector | Key Point |

|---|---|

| Barclays (BARC.L) | Global investment banking strength with diversified retail and corporate services |

| UBS Group (UBSG.SW) | Wealth management leader with strong presence in private banking and asset management |

| UniCredit (UCG.MI) | Italian retail & corporate banking with restructuring-driven profitability |

| BNP Paribas (BNP.PA) | Pan-European universal bank with strong capital markets and retail footprint |

| Commerzbank (CBKG) | Corporate lending and SME focus with digital transformation initiatives |

| Nordea Bank (Nordic Region) | Nordic resilience with strong retail and corporate banking across Scandinavia |

| Lloyds Banking Group (UK) | UK retail banking dominance with digital-first strategy |

| Crédit Agricole (France) | Cooperative banking model with strong insurance and asset management arms |

| Société Générale (France) | Diversified financial services with focus on cost efficiency and sustainable finance |

| ING Groep (Netherlands) | Digital banking pioneer with strong European retail presence |

10 Best Stocks or Sectors to Watch in European Banking & Finance

1. Barclays (BARC.L)

Headquartered in the UK and one of the UK’s largest banks, Barclays PLC specializes in investment banking, and offers a range of services in retail, corporate banking, and financial markets.

Barclays shares hit records in 2025, with strong trading income and an emphasis on maintaining a strategy of high-margin focus in fixed income and equities trading.

The bank has been returning cash to investors through buybacks and dividends, which further strengthens investors’ positivity around the bank. Barclays still has a number of challenges ahead and has not fully completed their legacy structural issues, such as the historical provisions of mis-selling.

However, Barclays is one of the most in transformed and the most relevant banks of the countless restructurings to be noted in the UK and European markets as they enter a changed environment.

Features Barclays (BARC.L)

Business Segmentation: The businesses are segmented into retail, corporate, and investment banking, covering the equities and fixed income trading businesses.

Capital Returns: The management policy of the bank focusing on return of capital via dividend payments and share buybacks policies.

Reorganization Goals: The strategic realignment to move toward higher-margin businesses.

Industry Dominance: The bank has a dominant position in the retail and commercial banking services in the UK which shelters the bank from income volatility.

| Pros | Cons |

|---|---|

| Strong UK retail and corporate franchise, with diversified investment banking operations. | Exposure to UK economic slowdown and legacy regulatory issues may impact profitability. |

| Significant shareholder returns via buybacks and dividends. | Sensitive to interest rate changes affecting lending margins. |

| Restructuring improves operational efficiency and higher-margin business focus. | Legal and historical mis-selling provisions remain a potential financial risk. |

| Well-positioned for growth in fixed-income and equities trading. | Competitive pressure from European and global banks. |

2. UBS Group (UBSG.SW)

UBS Group, the largest bank in Switzerland, is a worldwide frontrunner in wealth management and a considerable player in investment banking with a diversified business model.

After purchasing Credit Suisse, UBS is still in the phase of integrating its operations, while also widening the scope of its wealth and asset management.

This makes UBS a key player in making the European banking industry more competitive. However, even with the regulations proposed by the Swiss authorities, such as increased capital requirements, UBS is still advancing its investment banking revenues and cost efficiency.

This is a strategy that is most likely to land UBS in a premier position in the industry. UBS’s client orientation, along with the bank’s strong financial position, are the elements that have kept the bank profitable, and are the factors behind its growth.

This makes UBS a key player in the European financial services market and in the global financial services market.

Features UBS Group (UBSG.SW)

Industry Leader: The company is the largest wealth management company and private bank with significant asset under management, and thus has a large more diversified income.

Financial Flexibility: The company has a strong and well-structured capital balance, which provides a strong flexibility to absorb and withstand adverse market conditions.

Market Consolidator: The acquisition of Credit Suisse provides a larger market share and larger client portfolio in Europe.

Growth Opportunities: The company has a large income and a growing banking investment arm complementing the wealth management services.

| Pros | Cons |

|---|---|

| Leading global wealth management and investment banking presence. | Integration risk following Credit Suisse acquisition could create short-term disruptions. |

| Strong balance sheet and capital position, resilient to market shocks. | Regulatory scrutiny from Swiss and EU authorities may increase compliance costs. |

| Diversified revenue streams, including asset management and investment banking. | Market volatility can affect trading and advisory revenues. |

| Strategic growth in investment banking enhances long-term profitability. | High dependency on global financial markets and client wealth trends. |

3. UniCredit (UCG.MI)

UniCredit is the most extensive financial institution in Italy with a growing European presence, especially in Central and Eastern Europe.

The bank has made major strategic investments, such as significant purchases of Commerzbank shares, which increases UniCredit’s presence in the German financial market.

UniCredit profitability is remarkably diversified in corporate banking, retail, and capital market banking.

The bank’s digitalization, growing sustainable banking, and partnership with clients in different European markets underscores its growth potential. UniCredit ability to adapt and expand makes it stand out among European finance sector stocks.

Features UniCredit (UCG.MI)

Geographic Footprint: The company has a presence in Italy, and Germany, and has strong operations in Eastern and Central Europe.

Sector Leadership: The company offers corporate and retail banking and has a capital markets business.

Net Positive Banking: The company has made significant investments in digitization and in various projects with strong ESG credentials. The investment in digital banking and finance and in positive impact projects provides net positive long-term growth.

Strategic Partnerships: Enhances competitiveness and market presence through cross-border investments and acquisitions.

| Pros | Cons |

|---|---|

| Largest Italian bank with strong Central/Eastern European exposure. | Economic or political instability in Italy or Eastern Europe could impact performance. |

| Diversified services: corporate, retail, and capital markets. | Currency fluctuations in international markets can affect earnings. |

| Active M&A and strategic investments increase market footprint. | Integration risk from cross-border acquisitions. |

| Focus on digitalization and sustainable finance supports long-term growth. | Legacy loan portfolio risks may persist in volatile economic periods. |

4. BNP Paribas (BNP.PA)

Having a global presence in retail, corporate, and investment banking, BNP Paribas is one of the largest and most successful European banks.

The company recently reported having strong capital discipline and fundamentals and has raised shareholder returns, having adjusted capital targets.

BNP Paribas has many growing revenue streams, including wealth and asset management. The company also has made many successful and strategic acquisitions, strengthening its presence in the market.

BNP Paribas has a strong core capital and has excellent management of risks, which ensures the company will maintain its strength and resilience during challenging times. BNP Paribas is a complex and important European banking company.

Features BNP Paribas (BNP.PA)

Global Banking Leader: Major player in retail, corporate, and investment banking in Europe and globally.

Diversified Income Streams: Stable fee-based revenues come from both wealth and asset management.

Strong Capital Position: Well-capitalized and have regulatory requirements for when there are changes in the market.

Strategic Acquisitions: Increases presence and strengthens competitive position in several major financial markets.

| Pros | Cons |

|---|---|

| One of Europe’s largest banks with a strong global presence. | Exposure to EU regulatory changes and compliance costs. |

| Diversified revenue streams including retail, corporate, and wealth management. | Cyclical sensitivity in investment banking revenues. |

| Strong capital position and disciplined risk management. | Geopolitical or economic crises can impact cross-border operations. |

| Strategic acquisitions expand market reach and profitability. | Potential slowdowns in lending and capital markets activity. |

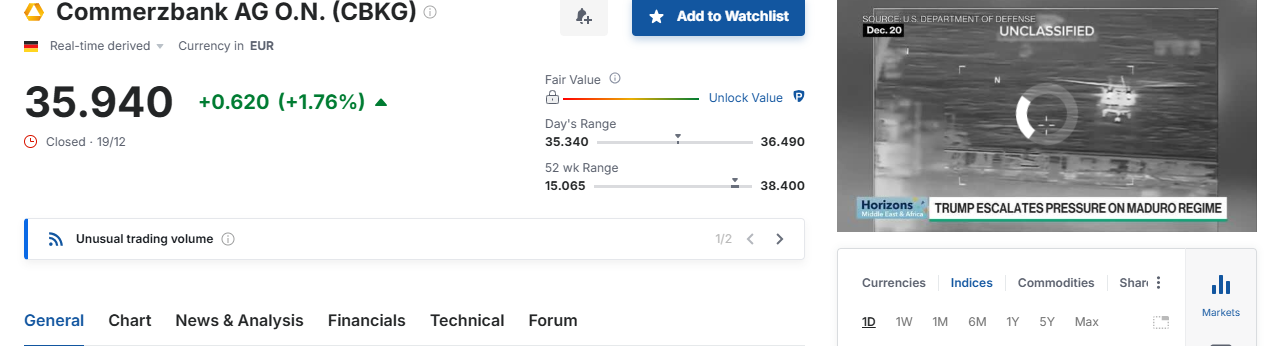

5. Commerzbank (CBKG)

Commerzbank, one of the largest private banking companies in Germany, has recently had some promising stock growth due to its operational development

As well as some outside strategic interest, most notably UniCredit, who recently acquired a large ownership position. Commerzbank’s most recent efforts focused on improving operational efficiencies and increasing revene growth.

The bank is interested in the profitability of the business given the strength of the German economy. The bank’s position in the stock market is of medieval Germany banking.

The bank is, and will continue to be, one of the most important German banks in the European wide stock market banking rally.

The bank will continue to be one of the most important German banks as the European trnede towards bank merger and consolidation is likely to continue.

Features Commerzbank (CBKG)

German Banking Strength: Notable retail and corporate banking player in Germany.

Cost Efficiency Focus: Improvement in operational efficiency increases profitability and sustainability in the long run.

Strategic Partnerships: Strengthens cross-border banking with a stake in UniCredit.

Sector Recovery Beneficiary: Will benefit from the positive sentiment from investors for the upcoming rally in European banking.

| Pros | Cons |

|---|---|

| Strong German retail and corporate banking presence. | Germany’s banking sector consolidation may increase competition. |

| Benefiting from improved investor sentiment and sector rally. | Limited geographic diversification compared to pan-European banks. |

| Strategic partnerships, including UniCredit stake, boost cross-border growth. | Sensitive to macroeconomic cycles and lending rates. |

| Cost-efficiency initiatives support profitability. | Historical loan and non-performing asset risks. |

6. Nordea Bank (Nordic Region)

As one of the region’s major financial institutions, Nordea Bank offers financial services to retail, corporate, and wealth management in Sweden, Finland, Norway, and Denmark, and enjoys stable earnings, high dividend yields, and a diversified Nordic economy.

Also, the Bank has a high capital base. However, Nordea’s digital transformation and risk management strategies provide a smooth operation in the face of rapid interest rate adjustments and volatile mortgage markets.

Owing to the conservative banking practices in the Nordic countries, Nordea has a low risk profile and a high return on assets, making them a candidate of interest on European banks watchlists.

Features Nordea Bank (Nordic Region)

Nordic Market Leader: Well-established in retail, corporate, and wealth management banking in the Nordic countries.

High Dividend Yield: Stable earnings make the bank attractive for investors seeking high dividends.

Digital Transformation: Operational efficiency and customer experience improvements are from technological investments.

Conservative Risk Management: Strong capital base and prudent lending limits the financial exposure.

| Pros | Cons |

|---|---|

| Leading Nordic bank with diversified retail, corporate, and wealth services. | Economic dependence on Nordic countries can limit global growth. |

| Stable earnings and high dividend yield attract income investors. | Regional exposure may be affected by currency and interest rate fluctuations. |

| Strong capital base and risk management practices. | Potential slowdown in mortgage and housing markets. |

| Digital transformation enhances operational efficiency. | Regulatory changes in the EU or Nordic countries may affect compliance costs. |

7. Lloyds Banking Group (UK)

Lloyds Banking Group is in first place among UK retail and commercial banks due to their dominant market share in mortgages, personal loans, and small business financing.

As Lloyds mainly operates in the UK, the bank has benefited greatly from credit conditions and deposit franchises.

Lloyds has a risk-averse approach when it comes to making money, and because of that, they’re able to pay their shareholders money.

Lloyds possesses a lot of freedom in their UK banking position. This is due to the firm’s size, the banking conditions, and their loyal banking customers. This gives the banking group a core position in the UK market.

Features Lloyds Banking Group (UK)

UK Retail Dominance: The market leader in providing mortgages, personal banking, and banking for small businesses.

Stable Credit Quality. Ensures strong profitability given a solid balance sheet.

Income-Driven Investment. High dividends are advantageous for long-term investors.

Conservative Risk Approach. Low exposure to global volatility enough to sustain a banking system within a domestic economy.

| Pros | Cons |

|---|---|

| Leading UK retail and commercial bank with strong market share. | Domestic focus increases exposure to UK economic downturns. |

| Strong deposit franchise and stable credit quality. | Sensitivity to interest rate cycles impacting lending margins. |

| Conservative risk management and consistent profitability. | Brexit-related regulations and market changes may add operational costs. |

| Attractive dividend potential for long-term investors. | Competition from fintechs and challenger banks. |

8. Crédit Agricole (France)

One of Europe’s largest cooperative banking institutions, Crédit Agricole, has significant involvement with regional and agri financing, infrastructure financing, and retail services.

Additionally, the bank has part ownership of Amundi, which is the asset manager with the greatest size in Europe and diversifies the bank’s income with fee-based services.

Being able to financially assist the economic network throughout France and the rest of the world is a strong consequence of compliances cooperative structure.

Because of the ever-changing nature of financial services, and the focus on climate and rural financing

The bank has made a strong commitment to providing community driven services and has created a positively differentiated role for themselves in the banking industry for years to come.

Features Crédit Agricole (France)

Cooperative Banking Strength. Deep regional presence and focus on agricultural and retail finance.

Diversified Operations. Ownership of Amundi strengthens asset management business.

Capital Stability. Financial performance of cooperative structure is strong and surplus.

Sustainability Focus. ESG initiatives and community-based financing.

| Pros | Cons |

|---|---|

| Large cooperative banking group with strong retail and agricultural finance. | Agricultural and regional focus may limit global growth opportunities. |

| Diversified income through Amundi asset management. | Exposure to European economic cycles affects loan demand and profitability. |

| Strong capital position and cooperative structure for stability. | Regulatory scrutiny on large European banks may increase operational costs. |

| Emphasis on sustainable and community-focused finance. | Integration of international operations may pose management challenges. |

9. Société Générale (France)

Société Générale is one of the top banks in France and its investment banking division is very strong. This bank also provides retail banking, asset management, and derivatives services.

In July, Systeme had a very strong performance in the sector and in the European stock rallies, winning arch in the sector and winning significant share prices.

The company’s commitment to digital risk adjusted growth with other competitors in the field of advanced digital finance platforms and ESG adjusted finance provides for a solid competitive position.

This solid base of capital and international reach made the company a true sector leader for other banks in Europe.

Features Société Générale (France)

Investment Banking Expertise. Strong capital markets, derivatives, and advisory.

Diversified Operations. Global presence complements retail, corporate, and asset management.

Digital & ESG Focus. Enhancing competitiveness with innovation and sustainable finance.

Capital Strength. Solid buffers against market volatility support capital resilience.

| Pros | Cons |

|---|---|

| Strong investment banking division with diversified services. | Volatility in capital markets can impact revenues significantly. |

| Solid capital buffers and international reach enhance resilience. | Regulatory changes and compliance costs can affect profitability. |

| Strategic focus on digital innovation and ESG finance. | Competition from larger pan-European banks in retail and corporate sectors. |

| Recent stock performance reflects strong operational execution. | Economic or political instability in European markets may pose risks. |

10. ING Groep (Netherlands)

ING Groep is a global bank based in the Netherlands, renowned for its efficient, technology-savvy retail and commercial banking.

With an emphasis on customer service and operational efficiency, ING offers commercial banking services at lower prices and has a leading digital banking platform with a low-cost structure.

Even with the margin pressures prevalent in other European banks, the strategic focus on digital transformation, and its extensive presence in significant European markets provides the bank with attractive long-term growth opportunities.

ING is modernizing banking in Europe with its focus on innovative digital lending, mobile banking, and expanded services in sustainable finance.

Features ING Groep (Netherlands)

Technology-Driven Banking. Strong digital for retail and corporate clients.

Operational Efficiency. Leaner structures improve profitability and reduce costs.

Sustainable Finance Commitment. Green lending and ESG-aligned products.

European Presence. Geographic diversity ensures strong market penetration and diversification.

| Pros | Cons |

|---|---|

| Efficient, technology-driven retail and corporate banking. | Margin pressures in European banking limit net interest income growth. |

| Strong digital banking platform enhances customer experience and reduces costs. | Exposure to European economic fluctuations affects lending performance. |

| Commitment to sustainable finance supports long-term growth. | Competitive pressures from global banks and fintechs. |

| Broad European presence in key markets provides diversification. | Sensitive to regulatory changes and capital requirements in the EU. |

How To Choose The Best Stocks or Sectors To Watch In European Banking & Finance

Financial Health & Stability Top-of-the-line balance sheets and capital, secure ratios, and a healthy presence of low performing loans and adequate liquid ratios.

Diversified Revenue Streams Best to target banks with a greater mix in their retail and corporate wealth management, as well as in their investment banking.

Market Position & Brand Top banks in their home market or with a pan European and even global presence tend to enjoy greater resiliency.

Dividend Yield & Shareholder Returns Companies demonstrating discipline and consistency through dividends and buy backs tend to have greater financial standing, as do their investors.

Growth Potential & Strategy Banks with digital, sustainable, and strategic acquisitions in budgeting to finance transformation tend to enjoy greater growth.

Economic & Regulatory Exposure Changes to the European Union or regional economies may drastically affect the direction and flow of interest rates. So one must understand how those will affect their overall performance.

Valuation & Risk-Reward Analyzing a company’s growth risk in the market, as well as their P/E and price to book ratios is essential to measuring their expected growth.

Conclsuion

In Conclusionn European banking and finance stocks provides some combination of safety, growth, and decent dividend payments.

Top tier banks such as Barclays, UBS, BNP Paribas, and ING have come to the fore due to their solid sheets, diversified income profiles, and strategic placement in the market.

Investors should look to the digital innovation, financial wellness, and trends in the sector to spot the best opportunities in Europe’s evolving financial landscape.

FAQ

Barclays, UBS, UniCredit, BNP Paribas, Commerzbank, Nordea, Lloyds, Crédit Agricole, Société Générale, and ING Groep.

Strong balance sheet, diversified revenue, consistent dividends, and growth strategy

Large-cap, well-capitalized banks with low NPLs are more resilient.

Both — many European banks offer stable dividends and long-term growth potential.

Rising rates can increase net interest margins, boosting profitability.

Yes, banks investing in technology and fintech integration often outperform peers.