This article will cover the Best Forex Execution Algorithms for Institutional Traders, specifically how VWAP, TWAP, POV and other algorithms assist institutions in completing large forex orders at most favorable prices while ensuring minimal impact on market.

- Key Points & Best Forex Execution Algorithms for Institutional Traders

- 10 Best Forex Execution Algorithms for Institutional Traders

- 1. VWAP (Volume-Weighted Average Price)

- 2. TWAP (Time-Weighted Average Price)

- 3. POV (Percentage of Volume)

- 4. Liquidity Seeking/Aggressive

- 5. Arrival Price

- 6. Implementation Shortfall

- 7. Arbitrage Algorithms

- 8. Adaptive Algorithms

- 9. Iceberg/Sliceberg

- 10. Stop-Loss/Take-Profit Hybrids

- How To Choose Best Forex Execution Algorithms for Institutional Traders

- Conclusion

- FAQ

So how do these drop executions reduce slippage and manage risk while optimizing execution performance across varied market conditions to capture better trading outcomes?

Key Points & Best Forex Execution Algorithms for Institutional Traders

VWAP (Volume-Weighted Average Price) Executes trades close to the average price weighted by volume, minimizing market impact and tracking benchmark performance.

TWAP (Time-Weighted Average Price) Splits orders evenly across a set time period to reduce timing risk and avoid large price spikes.

POV (Percentage of Volume) Trades a fixed percentage of market volume to blend into liquidity and reduce detection by other market participants.

Liquidity Seeking / Aggressive Algorithms Actively searches for available liquidity and executes quickly when favorable conditions appear, prioritizing speed over minimal impact.

Arrival Price Algorithms Focus on minimizing deviation from the price at order submission time, aiming to reduce slippage relative to entry price.

Implementation Shortfall Algorithms Optimize the trade-off between market impact and timing risk by minimizing the difference between decision price and execution price.

Arbitrage Algorithms Exploit price differences across markets or instruments to lock in risk-free or low-risk profit opportunities.

Adaptive Algorithms Dynamically adjust execution strategy based on market conditions like volatility, liquidity, and spread changes.

Iceberg / Sliceberg Algorithms Break large orders into smaller visible portions to conceal total order size and reduce market impact.

Stop-Loss / Take-Profit Hybrid Algorithms Combine execution with risk management by automatically executing trades when predefined loss or profit levels are reached.

10 Best Forex Execution Algorithms for Institutional Traders

1. VWAP (Volume-Weighted Average Price)

VWAP execution algorithms strive to achieve an average price per currency pair for a particular day weighted by trading volume.

These institutions also use VWAP at the time of placement for minimal market impact by executing orders in a participatory fashion relative to market liquidity.

This balances their trades towards more aggregated, less busy periods, leading to better execution and less slippage.

VWAP is a popular benchmark strategy because it represents their “fair value.” This is especially beneficial for large orders which would experience slippage, maximizing market average price versus a speed or aggressive execution.

| Pros | Cons |

|---|---|

| Minimizes market impact by aligning with market volume | May underperform in rapidly trending markets |

| Provides strong benchmark for execution quality | Not suitable for urgent or time-sensitive trades |

| Smooths large order execution over the trading day | Depends heavily on accurate volume prediction |

| Reduces slippage in liquid markets | Less effective in low-liquidity periods |

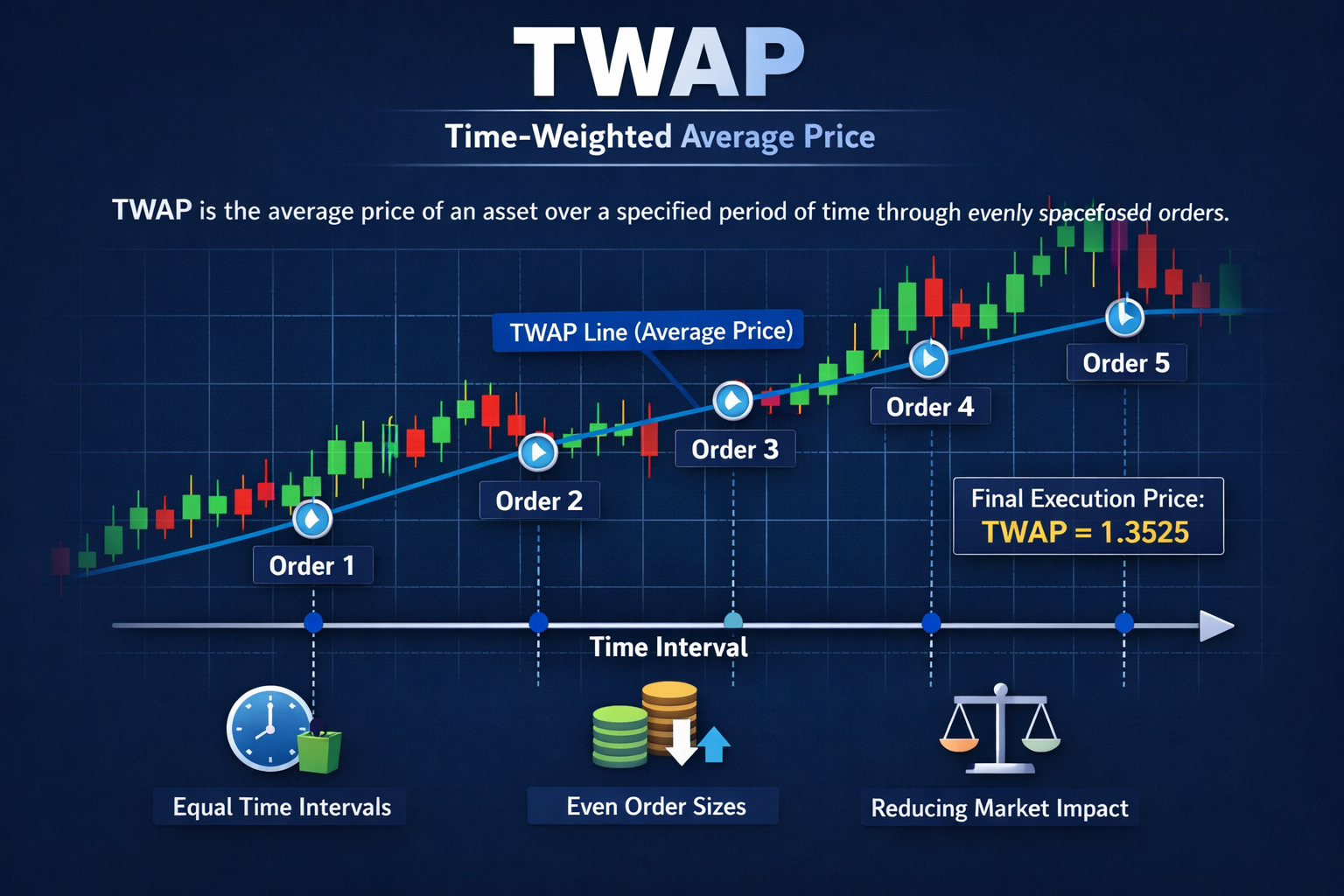

2. TWAP (Time-Weighted Average Price)

TWAP algorithms segment a large order into equal fractions executed at regular temporal intervals throughout a specified span of time.

TWAP is an execution strategy that is independent of volume and strictly time-based, unlike VWAP. This mitigates timing risk and prevents large trades from moving the market suddenly.

TWAP is employed by institutional traders when the volume of the market is unstable or they need an efficient and systematic execution strategy. It works best in stable and low-volatility markets.

TWAP, however, may not perform well in volatile scenarios since it does not respond to changing liquidity and can result in worse slippage than adaptive algorithms.

| Pros | Cons |

|---|---|

| Simple and easy to implement | Ignores market liquidity conditions |

| Reduces timing risk by spreading orders evenly | Can cause higher slippage in volatile markets |

| Useful in stable, low-volatility environments | May reveal trading intent if pattern is predictable |

| Ensures consistent execution over time | Not adaptive to sudden market changes |

3. POV (Percentage of Volume)

POV algos trade a set percentage of total market volume, like 5% or 10%. Execution speed is continuously patched based on real-time liquidity.

Execution speeds up when market volume increases and slows down when it decreases. This keeps the trader away from the touch and decreases price impact.

POV is best used for larger institutional orders that require a stealth execution. He is the one who seeks out urgent and discretionary tendencies

Which makes it very popular in forex markets where liquidity varies widely. This strategy allows traders to move with the natural flow of the market, without being detected by others.

| Pros | Cons |

|---|---|

| Blends into market activity for stealth execution | Execution speed depends on market volume |

| Reduces detection risk from other traders | Can be slow in low-volume conditions |

| Automatically adapts to liquidity changes | Less control over execution timing |

| Good for large institutional orders | May miss optimal price windows |

4. Liquidity Seeking/Aggressive

This form of trading encompasses liquidity-seeking algorithms which are strategically focused on querying multi-fold venues/order books available for ready-to-trade business opportunities.

These strategies are less concerned with reducing market impact and focus more on speed and certainty of execution.

Here, aggressive algorithms may cross spreads or submit market orders to trade immediately. Institutions employ them when urgency is acute, like during newsworthy events or volatility spikes.

They provide quick execution, but they can generate more slippage and higher trading costs. Such algorithms are critical in dynamic forex markets, where waiting for passive fills can result in missed opportunities or unfavourable price movements.

| Pros | Cons |

|---|---|

| Fast execution during high urgency situations | Higher transaction costs due to spread crossing |

| Captures fleeting market opportunities | Increased slippage risk |

| Accesses multiple liquidity sources quickly | Can move market against trader |

| Suitable for volatile/news-driven markets | Less price control |

5. Arrival Price

Arrival price algorithms optimize to minimize the distance from execution price and the same market price at the time of order placement.

The strategy keeps dynamically determining execution relative to this reference point as the market evolves.

It balances speed and impact dynamically, often executing trades more aggressively when price moves against the firm.

It is utilized by institutions to minimize slippage and execute with more cost efficiency. For benchmark-driven trading strategies, arrival price is a common parameter.

This approach is a good fit for moderately volatile markets where both timing risk and price deviation need to be managed prudently.

| Pros | Cons |

|---|---|

| Targets execution close to decision price | Requires continuous market monitoring |

| Reduces slippage compared to passive methods | Can increase urgency costs |

| Balances speed and market impact | Less effective in extreme volatility |

| Widely used benchmark strategy | Complex optimization logic required |

6. Implementation Shortfall

Implementation shortfall algorithms seek to minimize total cost when executing a trade relative to the decision price at the time the order was generated.

It accounts for all explicit costs (like fees, spreads) and implicit costs (such as slippage, market impact).

The algorithm reacts dynamically to balance urgency and price impact, typically filling faster when the risk is higher.

Institutional traders favor this way because it’s a more accurate representation of real-world trading costs than simpler benchmarks.

In portfolio execution, it is heavily relied upon. The idea is to minimize the “shortfall” between theoretical and actual execution performance, making it an incredibly sophisticated and commonly used execution strategy.

| Pros | Cons |

|---|---|

| Minimizes total trading cost (explicit + implicit) | Computationally complex |

| Accounts for slippage and market impact | Requires accurate risk modeling |

| Flexible execution strategy | Can be difficult to tune parameters |

| Industry-standard institutional benchmark | May over-optimize and slow execution |

7. Arbitrage Algorithms

Lastly, Arbitrage algorithms take advantage of price differences for currency pairs, brokers and markets. Do this, buying and selling assets at the same time, to lock in riskless or low-risk profit arbitrage.

In forex, ultra-low latency execution and high-frequency systems are the methods of choice to detect inefficiencies before they evaporate.

Arbitrage algorithms used by institutions in the spot, futures, and derivative markets Speed and accuracy are essential because arbitrage opportunities exist for just milliseconds.

Such algorithms help make markets efficient by correcting price discrepancies very quickly. But the competition is fierce, demanding sophisticated infrastructure and co-location to be profitable.

| Pros | Cons |

|---|---|

| Generates low-risk or risk-free profit opportunities | Extremely competitive environment |

| Improves market efficiency | Requires ultra-low latency systems |

| Works across multiple markets/instruments | High infrastructure cost |

| Can scale with high frequency trading | Opportunities exist for milliseconds only |

8. Adaptive Algorithms

Adaptive algorithms provide flexibility for adapting the execution strategy depending on real time market conditions such as volatility, liquidity and changes in spreads.

They can automatically become aggressive or passive depending market behavior. As an example, they might decelerate during illiquid periods and then go faster when liquidity is high.

Adaptive algorithms used by institutional traders to maximize the efficiency of their execution and lower trading costs.

They typically use machine learning or statistical models to enhance decision-making. The best strategies are highly adaptive and outperform less flexible static strategies in unpredictable fx regimes, making them a foundational component of any modern algorithmic trading system.

| Pros | Cons |

|---|---|

| Adjusts dynamically to market conditions | Complex model design and maintenance |

| Reduces execution risk in volatile markets | Requires high-quality real-time data |

| Uses AI/ML for improved decision-making | Risk of model overfitting |

| Efficient across different market regimes | Hard to predict behavior in extreme events |

9. Iceberg/Sliceberg

Iceberg or sliceberg algorithms chop a large order into multiple smaller visible ones and shield the total order size.

If an order is masked, a small percentage of the order will show up on the market at any point in time to avoid market impact or front-running.

New orders are released automatically as each portion fills. Institutional traders implement this practice to place outsized positions without signaling their intent as a whole.

This is especially helpful in low-liability forex pairs. Such a technique keeps price steady and allows the investment to be made gradually over time.

| Pros | Cons |

|---|---|

| Hides full order size from the market | Slower full execution of large orders |

| Reduces market impact and front-running risk | Partial fills can create inefficiency |

| Improves execution stealth | Requires careful order management |

| Suitable for low-liquidity pairs | May expose pattern over time |

10. Stop-Loss/Take-Profit Hybrids

Stop-loss and take-profit hybrid algorithms automatically execute risk management. They trigger trades automatically as soon as preset price levels are reached, either to limit losses or lock in profits.

Instituting these into execution systems help manage downside risk of donks while locking in gains. Moreover, These algorithms can also be dynamically varied based on volatility or market conditions.

They are critical for exercising disciplined trading and also protecting capital when unexpected volatility occurs.

Hybrid systems, which rely on both execution and risk control principles, ensure that trades are opened only when certain thresholds of profit or loss are met, thus improving the aggregate strategy performance.

| Pros | Cons |

|---|---|

| Automates risk management | Can trigger during short-term volatility spikes |

| Protects capital from large losses | May exit trades prematurely |

| Locks in profits systematically | Limited flexibility in fast-changing markets |

| Reduces emotional trading bias | Requires precise level setting |

How To Choose Best Forex Execution Algorithms for Institutional Traders

Analyze Order Size VWAP, POV (percentage of volume) or iceberg algorithms for large orders; aggressive or liquidity-seeking execution for smaller orders.

Consider Market Liquidity VWAP and POV work in high liquidity − Adaptive or iceberg strategies are better for lower liquidity

Evaluate Market Volatility Adopt adaptive or implementation shortfall algos in volatile markets to dynamically adjust execution.

Prioritize Execution Speed Liquidity-seeking or aggressive algorithms are best for urgent trades or news events.

Focus on Slippage Control If speed is less important than minimizing slippage, choose VWAP, TWAP or arrival price algorithms.

Assess Trading Costs Total trading cost, which measures the effectiveness of Algorithms To Personalize your sales funnel

Check Strategy Complexity Straightforward strategies such as TWAP are easily manageable, whereas adaptive algorithms demand complex housed systems.

Conclusion

Lastly, the selection of suitable Forex execution algorithms impact optimal trading performance in institutional traders.

By ideally mixing the VWAP, TWAP, POV and adaptive strategies, such strategies provide a good balance between cost efficiency (of execution), speed of execution, and market impact.

Traders can reduce slippage, increase execution quality, and ultimately maximize total returns on their portfolios in extremely competitive

forex markets by tuning algorithms to the liquidity available during different price levels based on market conditions including volume flow (liquidity), volatility, and order size.

FAQ

Arrival price algorithms aim to execute trades close to the price at the time the order is placed, reducing slippage.

These algorithms actively search multiple liquidity pools and execute trades quickly, often prioritizing speed over minimal cost.

TWAP executes orders evenly over time, while VWAP executes based on volume distribution, making TWAP simpler but less adaptive to liquidity.

Adaptive algorithms adjust execution strategies in real-time based on market conditions like volatility, spread, and liquidity.