In this article, I would like to present some reasons as to why the Bank of Canada might be finished policy rate cuts; at least for now. While the most recent rate cut brought some relief to borrowers, the economy still warrants a pause.

- Introduction

- The Rate of Inflation is Less of a Concern for the Economy

- Canada’s Stronger Economic Data

- Slower Growth in the Canadian Labour Market

- A Global Stance of Caution from Central Banks

- Volatility in the Financial Market

- Household Debt Worries

- Still Monitoring Early Indicators

- Political as well as Societal Expectations

- Conclusion

- FAQ

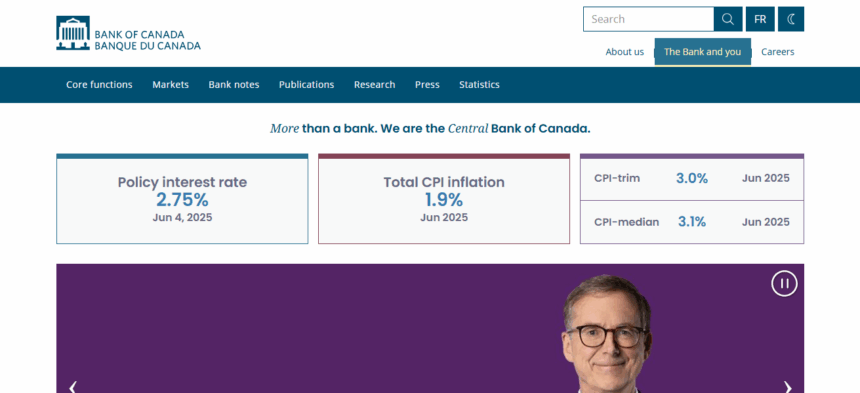

Given the lingering above-target inflation and relatively strong economic performance, the central bank seems likely to lean toward a more cautious, wait-and-see approach.

Introduction

It appears that the Bank of Canada (BoC), following a carefully orchestrated sequence of aggressive policy hikes to tame inflation and a cautious rate cut in June 2025, is now likely to press pause on further reductions to the policy interest rate.

Data available until the recent June 2023, and June 2023 data indicated a rebound in economic activity suggested room for cuts but recent evidence shows a move towards stabilization. Therefore, a large section of the analysts feel that the Bank is done with rate cuts for now.

The Rate of Inflation is Less of a Concern for the Economy

The persistent nature of inflation is a fundamental driver of this change. The core inflation rate peaked in 2022 and has been consistently falling past 2 percent for a sustained period.

The inflationary impact on the economy services sectors, and the roof over their head considerably support the theory of inflation risks, faulty economic policies and bad governance. Moreover, the devils like cutting too much and too fast will allow destruction of skeletal services to flourish in the guise of real services.

Canada’s Stronger Economic Data

The Canadian economy has proven more resilient than it has been in the past. The most recent job numbers have held steady, and while consumer spending is decelerating, it is not in freefall.

The housing market is also waking up after a period of cooling earlier in the cycle. These factors mitigate the need for further rate cuts, particularly as the intended goal of such cuts is already being partially achieved.

Slower Growth in the Canadian Labour Market

Despite the slight rise in unemployment, it is still achieved a record low in the last decades. The inflationary landscape is further complicated as wage growth remains steady.

The BoC (Bank of Canada) may see this as reasoning that the economy does not require financial stimulus. Labour market equilibrium typically has the opposite effect, encouraging rate cuts.

A Global Stance of Caution from Central Banks

Global issues also matter. The US, European, and English central banks all seem to be striking a cautious tone, maintaining a status quo or minimal cuts to their own.

Canada cannot risk a more aggressive cut offset to potential weakening of Canadian dollar and inflation. From this, the BoC is more constrained in their decision making.

Volatility in the Financial Market

Recent months have experienced increased volatility in financial markets as global equities face sharp shifts and the bond markets respond vigorously to central bank cues.

In these circumstance, the Bank of Canada may want to keep policy settings unchanged. An unexpected cut in the key rate may disrupt markets or signal misplaced central bank confidence in the economy.

Household Debt Worries

The central restraining policy comes from Canada’s high household debt figures. With Canada’s high household debt, lower rates may ease debt burden in the short-run, but in the long-run, it may allow more borrowing which can lead to unsustainable credit growth especially in the housing sector.

The central bank likely would want to see the impact of the prior rate reductions on household behavior before adding more stimulus to the economy.

Still Monitoring Early Indicators

The Bank of Canada appears to be keeping its balance and have pledged to be data-driven. There’s a possibility that the Bank of Canada prefers to monitor the effect of the June rate cut in the coming months before responding to the markets.

Given the sluggish pace of monetary policy impact, the full consequences of earlier actions may not yet be apparent. This affords the Bank of Canada the option to be on the sidelines.

Political as well as Societal Expectations

The scrutiny from politicians as well as the general public are both changing policies of the bank. The BoC, for example, will not want to seem to be influenced by outside forces in the leadup to the year 2025 elections.

By keeping rates on hold, the bank reinforces the image of an undistracted, balanced institution that focuses on long-term stability instead of short-term popularity.

Conclusion

To conclude, the Bank of Canada seems to be done easing for the time being, even though the possibility for future cuts still exists. The enduring inflation, resilient economy, careful global peers, and prevailing financial stability concerns all warrant the pause.

It seems the bank’s most prudent strategy for now is to hold rates on standby while carefully observing the consequences of previous decisions to inform future ones.