This article identifies the Best Low-Risk Investment Opportunities in Asia for conservative investors that are safe and provide predictable returns.

- Key Points & Best Low-Risk Investment Choices In Asia

- 10 Best Low-Risk Investment Choices In Asia

- 1. Fixed Deposits (FDs)

- 2. Public Provident Fund (PPF)

- 3. National Savings Certificates (NSC)

- 4. Government Bonds

- 5. Post Office Savings Schemes

- 6. Recurring Deposits (RDs)

- 7. Debt Mutual Funds

- 8. Unit Linked Insurance Plans (ULIPs)

- 9. Gold ETFs

- 10. Employee Provident Fund (EPF)

- How To Choose The Best low-Risk Investment Choices In Asia

- Conclusion

- FAQ

This includes government schemes, fixed deposits, and other debt instruments that keep your money safe and produce income. These are perfect for anyone looking to finances for the short and/or long-term.

Key Points & Best Low-Risk Investment Choices In Asia

| Investment Choice | Key Point |

|---|---|

| Fixed Deposits (FDs) | Guaranteed returns with low risk, offered by banks across Asia. |

| Public Provident Fund (PPF) | Government-backed savings scheme with tax benefits and long-term security. |

| National Savings Certificates (NSC) | Safe fixed-income option backed by government, ideal for small investors. |

| Government Bonds | Stable returns with sovereign guarantee, suitable for risk-averse investors. |

| Post Office Savings Schemes | Accessible and secure investment with fixed interest rates. |

| Recurring Deposits (RDs) | Disciplined savings with monthly deposits and assured returns. |

| Debt Mutual Funds | Low volatility funds investing in bonds and money market instruments. |

| Unit Linked Insurance Plans (ULIPs) | Insurance + investment with moderate risk and tax benefits. |

| Gold ETFs | Safe hedge against inflation with liquidity and transparency. |

| Employee Provident Fund (EPF) | Retirement-focused savings with employer contribution and government backing. |

10 Best Low-Risk Investment Choices In Asia

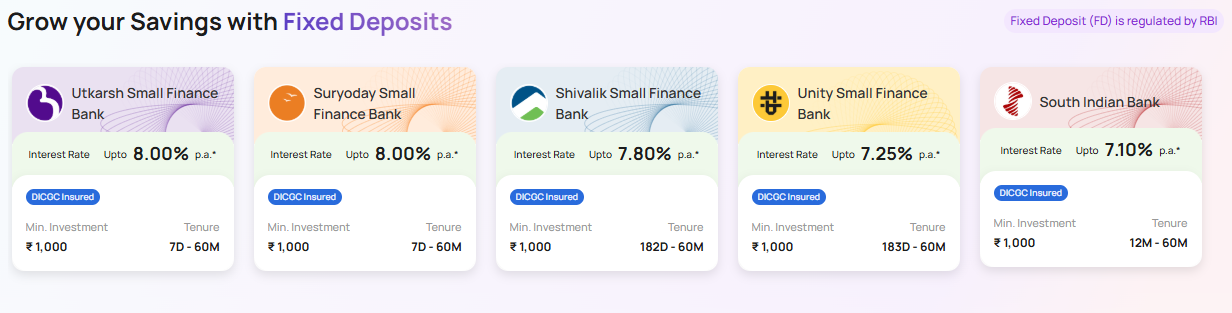

1. Fixed Deposits (FDs)

A fixed deposit is also known as an FD, and is considered to be one of the safest investment opportunities from the bank and other financial institutions.

Investment is for a lump sum for a fixed period of time, and the interest rate is fixed and is higher than a savings account.

In an FD, the principal amount is guaranteed, making it a low risk investment option. The interest can be paid out in a flexible manner as to how the investor pleases, including monthly, quarterly, annually, or one time at the maturity date.

FDs are also an option for those seeking to invest conservatively, as the principal amount is guaranteed, and there is likeliness to receive interest in at maturity date.

In Asian countries, it is also a benefit to deposit savings within a tax-saving FD, as they are usually paired with a government scheme.

Features Fixed Deposit (FD)

Guaranteed Returns – You will receive the principal, and the interest rate is guaranteed for the period.

Flexible Tenure – Ranges from a few months to a few years of the stated period.

Interest – You can choose to receive the interest monthly, quarterly, annually, or all at once at the end of the period.

Loan – You can take a loan from the bank, using the deposit as collateral.

| Pros | Cons |

|---|---|

| Guaranteed returns with principal safety. | Interest rates may be lower than inflation, reducing real returns. |

| Flexible tenure options (short-term to long-term). | Premature withdrawal may attract penalties. |

| Available at banks and financial institutions nationwide. | Taxable interest can reduce net returns. |

| Can be used for loan collateral in some banks. | Returns are fixed; no scope for higher gains during market upswings. |

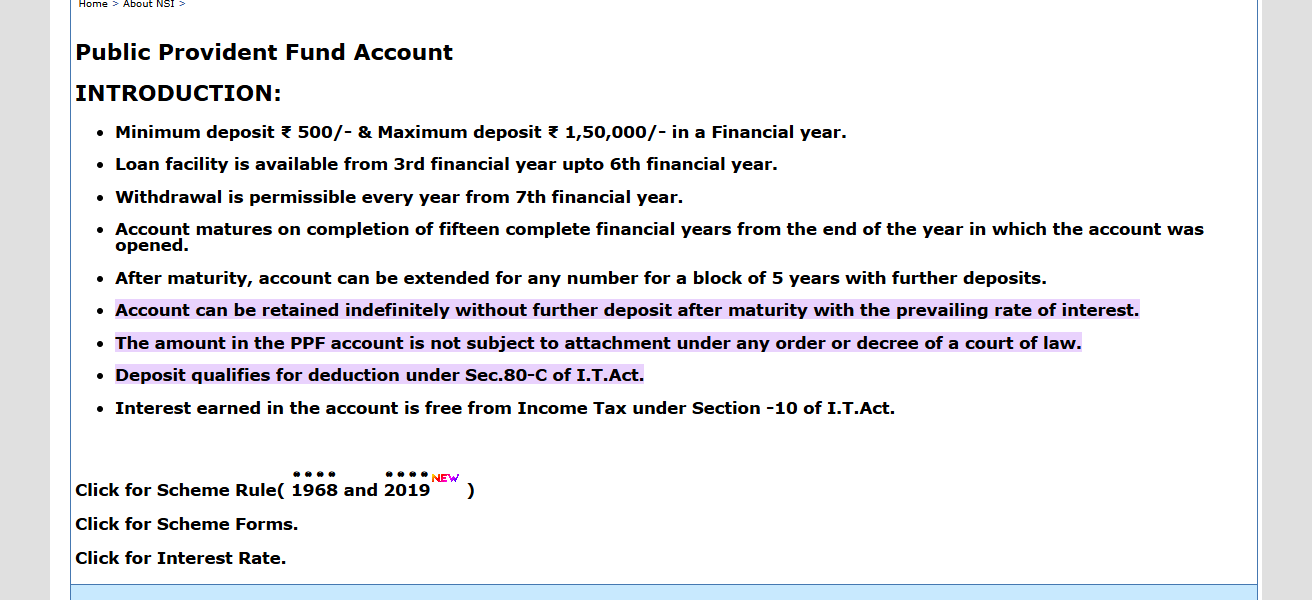

2. Public Provident Fund (PPF)

The government supports the Public Provident Fund as the most low-risk long-term savings scheme available.

The PPF has annual interest rates that are compounded with tax-exempt returns. Its 15 Lock-in period encourages long-term disciplined savings.

After a few years withdrawals are allowed giving limited immediate access. It is excellent for investors who are averse to risk and are seeking guaranteed growth for retirement.

Its safety and the tax benefits have made the scheme one of the most popular across several Asian nations. PPF is especially popular in India.

Features Public Provident Fund (PPF)

Guaranteed government backing – The government guarantees the principal as well as the interest.

Long Term Saving – The saving is for a period of 15 years, but can be extended to blocks of 5 years at a time.

Taxes – The contributions made into the fund are tax deductible, and there is tax exemption for the interest earned.

Withdrawals – There is allowance for some withdrawals of the principal after a few years to provide for emergencies and other major expenditures.

| Pros | Cons |

|---|---|

| Government-backed, extremely safe investment. | Long lock-in period of 15 years. |

| Tax-free interest and eligible for tax deduction under certain sections. | Limited liquidity; partial withdrawals allowed only after specific years. |

| Encourages long-term disciplined savings. | Returns may fluctuate slightly with government-set interest rates. |

| Can be extended beyond maturity in 5-year blocks. | Not suitable for short-term goals due to long tenure. |

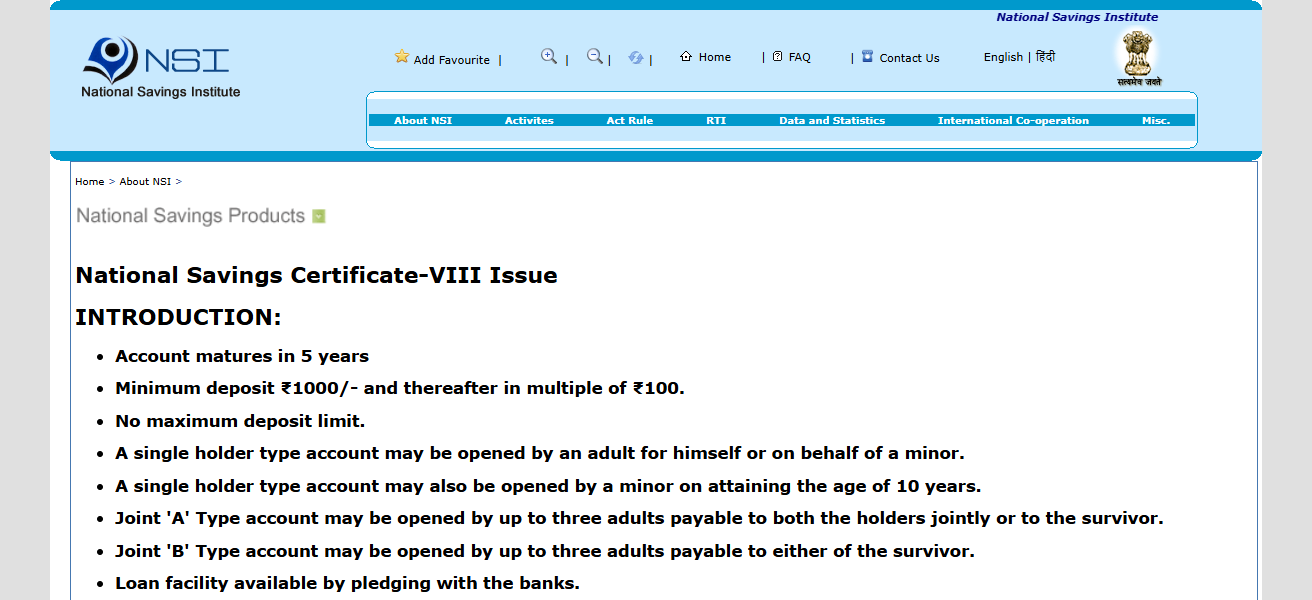

3. National Savings Certificates (NSC)

National Savings Certificates are fixed income and government-backed investment tools that are predominantly sold through post offices.

These options have a fixed maturity of five and ten years and have an annual interest compounded.

There is complete safety on the principal investment because of the government backing, making it a very low risk option.

While the interest earned would be taxed, the investment would qualify for some tax deductions under select sections within the local tax law.

This investment is available for small investors, as the initial investment is very minimal. This would be best for very conservative investors

Who are looking for a sure way to earn returns while also saving on tax. Other than the specific situations, it is very illiquid as it does allow for premature encashment.

Features National Saving Certificates (NSC)

Government Backed – Investment is relatively risk-free, as it is provided and backed by the government.

Fixed Tenure – Espcially 5 and 10 years are the most common time period options.

Taxes – There are some tax benefits offered for investing in this option; the investment made qualifies for some deductions.

Compounding of Interest – There will be interest, and it is compounded on an annual basis. The interest is not paid until the end of the period.

| Pros | Cons |

|---|---|

| Principal and interest are guaranteed by the government. | Interest earned is taxable. |

| Small initial investment required; accessible to everyone. | Tenure is fixed; limited flexibility. |

| Eligible for tax deduction under certain tax sections. | Premature withdrawal allowed only under specific circumstances. |

| Safe and low-risk investment for conservative investors. | Returns may be lower than market-linked instruments over long term. |

4. Government Bonds

Government bonds are issued by the national or state governments through the issuance of government bonds. For one, it is one of the safest investments since the principal is guaranteed.

A bond will pay interest, is in the form of coupons, and returns the principal when the bond matures.

An investor can choose to have either a short term of long term bond, government bonds can also be traded in the secondary market for investors that need that liquidity.

For those conservative investors that want predictable income and want to diversify their portfolios, normally want their portfolio with a low credit risk.

In Asia, these government bonds are used with a preference when there are any regulations regarding the economy since it will be stable with guaranteed returns.

Features Government Bonds

Guaranteed principal – Along with it being issued by the government, the principal is also guaranteed as well to the bond holder by the government

Steady Income – Pays coupons on a regular basis.

Tradability – Can be traded on secondary markets before maturity.

Variety of Tenures – Available in a wide range of maturities to accommodate different objectives.

| Pros | Cons |

|---|---|

| Principal is backed by the government; extremely safe. | Returns are moderate and may lag behind equities. |

| Provides periodic interest (coupon) payments. | Long-term bonds are subject to interest rate risk. |

| Tradable in the secondary market for liquidity. | Market price may fluctuate if sold before maturity. |

| Suitable for portfolio diversification and stable income. | Not ideal for short-term capital gains. |

5. Post Office Savings Schemes

Savings plans offered by the Post Office like savings accounts, monthly income plans and fixed deposits, are government-backed, low-risk investment options that make it possible for individuals to grow savings with little interest.

Conservative investors and older individuals looking for additional income would find these perfect. It is common for interest rates to be fixed and certain plans to have available tax incentives.

Other than the interest rates, these plans are easily accessible since post offices are located in every urban and rural area.

Because these plans are safe and reliable, with low-cap investment options, they have become a popular choice for low-risk investors all over Asia.

Features Post Office Savings Schemes

Government Security – Offers safety and low-risk investment.

Multiple Schemes – Available in savings, recurring, monthly income, and time deposit variants.

Widely Available – Accessible via both urban and rural post offices.

Tax Benefits – Some schemes offer tax-deduction benefits.

| Pros | Cons |

|---|---|

| Government-backed; extremely low-risk. | Interest rates may be lower than banks’ FDs in some cases. |

| Accessible across urban and rural areas. | Limited investment amounts for some schemes. |

| Some schemes offer tax benefits. | Premature withdrawals may be restricted. |

| Multiple options: savings, monthly income, time deposits. | Returns are fixed; no potential for higher market-linked gains. |

6. Recurring Deposits (RDs)

A bank or post office account may offer Recurring Deposits (RDs) as a method of disciplined saving. Investors make a monthly deposit for a predetermined number of months.

Interest is earned monthly and is added to the principal. Interest rates on bank RDs are higher than a typical bank saving account.

RDs are low risk since interest on the total principal is added monthly. The ability to successively increase the interest earned on the principal makes RDs ideal for salaried people and people with steady monthly income.

There is a penalty for early withdrawal. RDs are a popular method of saving for conservative and disciplined investors in Asian countries because the income earned is guaranteed.

Features Recurring Deposits (RDs)

Disciplined Savings – Monthly installments cultivate a habit of savings and investments.

Interest Rate – Higher than traditional savings accounts.

Tenure – Flexible, ranging from 6 months to 10 years.

Penalties – Applied on early withdraw, which is otherwise allowed.

| Pros | Cons |

|---|---|

| Encourages disciplined, regular savings. | Premature withdrawal may attract penalties. |

| Principal is safe; interest rate higher than savings accounts. | Interest is taxable, reducing net gains. |

| Flexible tenure options (6 months to 10 years). | Fixed returns; no opportunity to benefit from market growth. |

| Easy to open in banks and post offices. | Inflation may erode real returns for long-term RDs. |

7. Debt Mutual Funds

Debt mutual funds invest in fixed – income securities like corporate bonds, money market instruments, and government bonds. They are less volatile compared to equity funds.

They also offer slight returns with comparatively less risk. Investors get to enjoy professional fund management and diversification across various debt instruments.

For short-term objective goals, debt funds can be part of a balanced portfolio to reduce overall risk. They offer liquidity compared to traditional fixed deposits and provide certain tax benefits under long-term capital gains.

These funds are a good fit for conservative investors that are trying to achieve consistent and stable returns with little market fluctuations.

Features Debt Mutual Funds

Low Risk – Investment is in government/corporate bonds and money market instruments.

Management – Done professionally, with expert fund managers.

Liquidity – Accessible any time, which is not the case with FDs or PPF.

Risk Mitigation – Through diversification. Risk is further minimized by spreading the investment over a range of different debt instruments.

| Pros | Cons |

|---|---|

| Low risk compared to equity funds; moderate returns. | Returns are not guaranteed; value may fluctuate slightly. |

| Professional fund management and diversification. | May be subject to interest rate and credit risk. |

| More liquid than traditional FDs; can be redeemed anytime. | Short-term capital gains are taxable. |

| Suitable for conservative investors with short to medium-term goals. | Lower returns compared to equities in a bullish market. |

8. Unit Linked Insurance Plans (ULIPs)

Unit Linked Insurance Plans intertwine insurance along with investment as one product. Certain sum of the premium secures the policy insurance, whereas the balance is allocated to funds, debt or equity, and also depends on the risk appeal of the insurer.

ULIPs with debt orientation has little to no risk and presents equitable returns, however in the equity focused approach

There is always risk involved. Under legal regulations in place, ULIPs presents opportunity for regulation of payment, and also offers tax exemptions.

These plans are the most favorable option for long term financial goals, or even retirement funds Wealth creation is guaranteed with insurance.

More conservative investors should happily select debt focused ULIPs for protection of insurance along with calm, consistent growth.

Features ULIPs

Double Advantage – Investing along with an insurance cover.

Allocation Flexibility – Choose any of the equity, debt, or balanced funds.

Tax Benefits – Premiums and proceeds earned are exempted.

Gradual Investment Growth – Disciplined investing for years.

| Pros | Cons |

|---|---|

| Combines investment and insurance in one plan. | Charges and fees can reduce returns in initial years. |

| Debt-oriented ULIPs provide low-risk, stable returns. | Returns depend on market performance if equity-linked. |

| Tax benefits on premiums and maturity proceeds under applicable laws. | Lock-in period of 5 years limits liquidity. |

| Systematic investment helps long-term wealth creation. | Complex structure may confuse novice investors. |

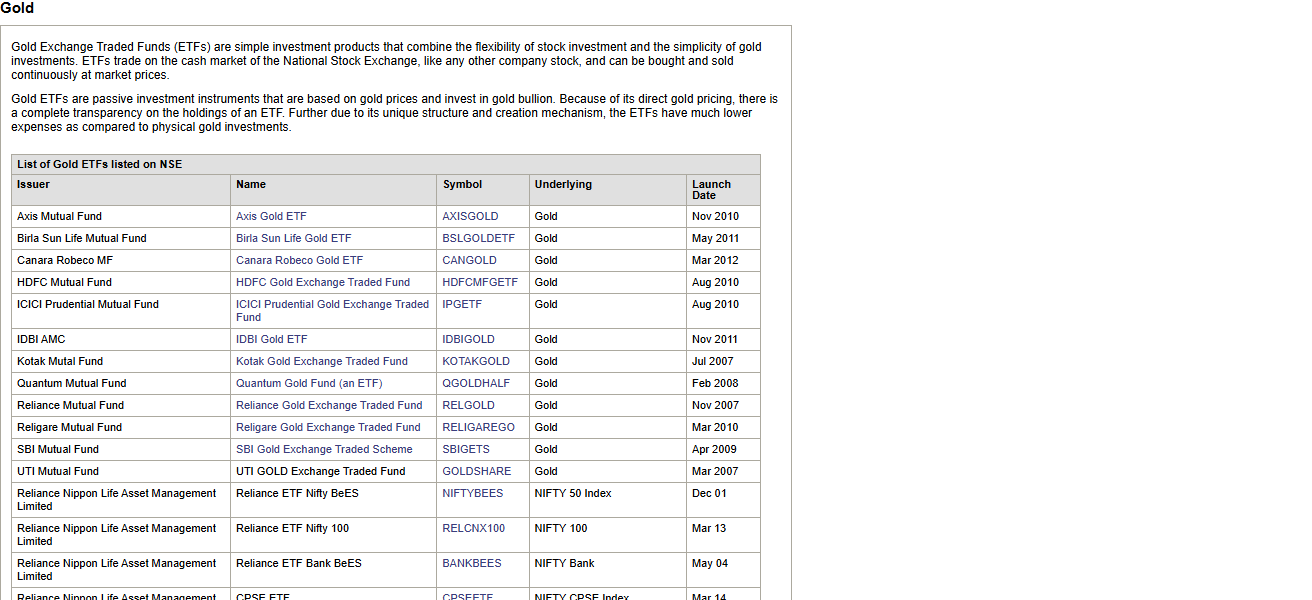

9. Gold ETFs

Gold Exchange Traded Funds (ETFs) provide a way for investors to get exposure to holding gold without having to store gold physically.

Gold ETFs follow the gold market price, providing liquidity along with transparency. With gold, you do not have to worry about the risks of having gold, such as theft and storage.

In equities, these funds do have low risk, but gold fluctuations can happen. Investors can buy and sell them anytime on the stock.

Gold ETFs were made for protecting wealth and for diversifying a portfolio against inflation. In Asia, conservative investors looking for a stable store of value and inflation protection these have become very popular.

Features Gold ETFs

Gold Investment – Purchase gold without the hassles of gold possession.

Easy Accessibility – Easily bought and sold on the stock exchange.

No Risk of Theft – No problem without gold possession.

Diversified Portfolio – Currency fluctuations and inflation are hedged.

| Pros | Cons |

|---|---|

| Provides exposure to gold without physical storage risk. | Prices fluctuate with global gold market; not guaranteed. |

| Highly liquid; traded on stock exchanges. | Brokerage fees apply during buying/selling. |

| No risk of theft or storage costs like physical gold. | Returns may be lower than other long-term investments. |

| Helps diversify portfolio and hedge against inflation. | Market volatility may affect short-term performance. |

10. Employee Provident Fund (EPF)

Employers and employees contribute every month a percentage of salary to a Employee’s Pension Scheme fund with every month. This is an optional pension fund.

EPF invests this money and offers a guaranteed and safe return. This is a low-risk profile. EPF contributions qualify for tax-deductible contributions and earned interest on these accounts is tax-free up to a specific point.

Employee’s valid reasons to withdraw money from these employs include retirement, medical emergencies, and housing.

EPF ensures participants save money over the long and medium term, while also ensuring staff financially safe in retirement.

This scheme is utilized in a majority of Asian countries, most notably in India. This is a trustworthy and low-risk option for salaried employees.

Features EPF

Risk-Free – Government security with almost zero risk.

Fixed Employer Contribution – A fixed percentage of salary from both the employer and employee.

Tax-Free Interest – Interest and contributions are exempted under certain limits.

Encouraged Retirement Savings – Savings post-retirement.

| Pros | Cons |

|---|---|

| Government-backed and very low-risk. | Limited access to funds before retirement, except for emergencies. |

| Provides tax-free interest and tax deductions on contributions. | Returns are fixed by government; may lag inflation. |

| Promotes disciplined, long-term retirement savings. | Contribution is mandatory for salaried employees in some countries. |

| Partial withdrawals allowed for housing, medical emergencies, or education. | Not ideal for short-term investment goals due to lock-in. |

How To Choose The Best low-Risk Investment Choices In Asia

Assessing One’s Risk Tolerance: Stick to the low-risk investment options that will align and not exceed your risk comfort level. The safest option will be the government-backed instruments.

Checking the Possible Returns: You will need to go through low-risk investment instruments and check the diversification interest rates, dividends, and the overall growth for your investments.

Assessing Investment Liquidity: You will want to ensure that you can freely access the funds whenever your needs arise as investment options could lock in your funds for a period of time.

Assessing Investment Tenure: The investment duration you choose to go with will need to align with your overall financial objectives and goals whether they be on the short-term horizon or the long-term horizon.

Loss of Taxable Money: Some investment schemes will be beneficial to you in that they can give you a deduction or interest that will not be taxable.

Portfolio Diversification: Flexible instruments with low-risk investments will allow you to be able to spread your investments.

Conclusion

In summary, the Best Low-Risk Investment Choices in Asia guarantee safety, financial stability, and a sense of security. FDs, and PPF, NSC, and government bonds as well as EPF all act as safe havens while allowing for the generation of consistent returns.

Investors who take into account their risk tolerance, tenure, liquidity, and tax implications/benefits of certain assets, including EPF act, will ultimately be able to build a robust financial portfolio.

FAQ

Low-risk investments are financial instruments that prioritize capital safety and provide stable returns with minimal chance of loss.

Government-backed schemes like PPF, NSC, EPF, and government bonds are considered the safest.

Yes, FDs offer guaranteed returns with principal safety and flexible tenure options.

Yes, options like PPF, NSC, EPF, and certain FDs provide tax deductions and tax-free interest.

Liquidity varies: FDs, RDs, and gold ETFs are more accessible, while PPF and EPF have long lock-in periods.